CP 575 Course Day 26 Post

Day 26: Tax Planning Considerations – Partnership vs S-Corp vs C-Corp

Choosing the right tax classification for an LLC is not just about filing the correct IRS forms—it is a strategic decision that directly affects tax savings, audit risk, administrative workload, and long-term business goals. Day 26 focuses on understanding how to evaluate whether your LLC should remain a partnership, elect S-Corporation, or opt for C-Corporation taxation.

This lesson will give you a simple, practical way to compare all three options using tax planning principles—especially relevant when reviewing your Notice CP 575 and determining if changes are needed.

Understanding the Three Taxation Paths for LLCs

LLCs are flexible because they can choose among three different tax treatments. The best option depends on ownership structure, profit levels, reinvestment goals, and compensation needs.

Below is a breakdown of when each classification makes sense.

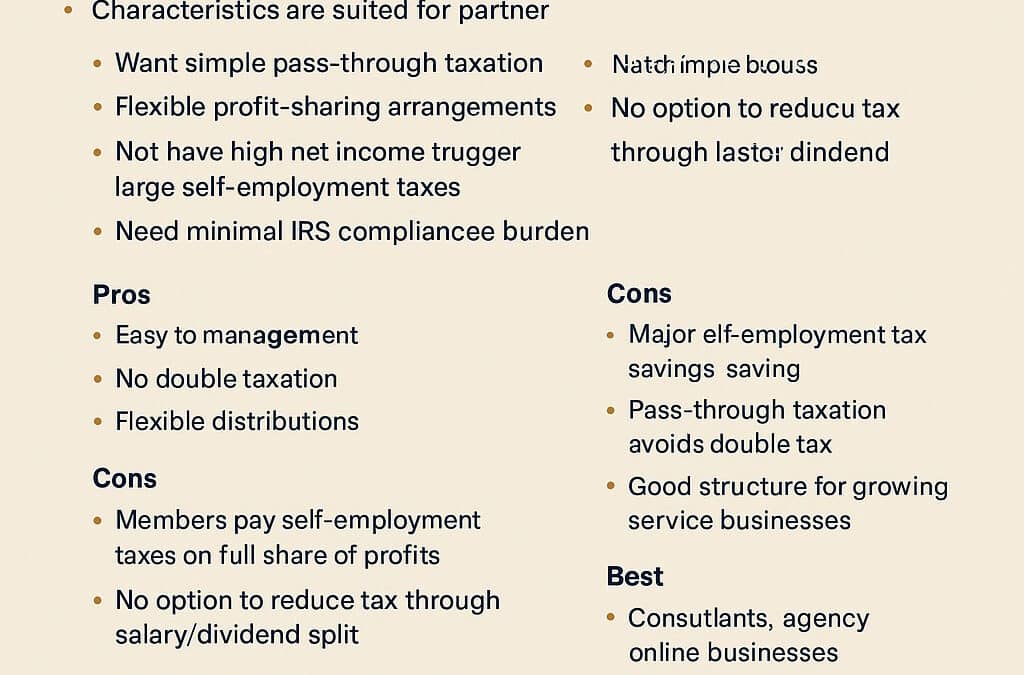

1. Partnership Taxation (Form 1065)

Default for multi-member LLCs.

Partnership taxation usually fits LLCs that:

• Want simple pass-through taxation

• Prefer flexible profit-sharing arrangements

• Do not have high net income that would trigger large self-employment taxes

• Need minimal IRS compliance burden

• Have members actively involved in the business

Pros:

• Easy to manage

• No double taxation

• Flexible distributions

Cons:

• Members pay self-employment tax on full share of profits

• No option to reduce tax through salary/dividend split

Best For: Startup LLCs, small partnerships, and businesses with moderate profits.

2. S-Corporation Taxation (Form 1120-S)

Best for LLCs with consistent profits and owners actively working in the business.

S-Corp works well for LLCs that:

• Have at least moderate profits ($40,000+ per owner annually)

• Want to reduce self-employment taxes

• Can justify a “reasonable salary” to owners

• Want pass-through taxation without partnership SE tax burden

• Do not plan to bring on foreign owners or multiple ownership classes

Pros:

• Major self-employment tax savings

• Pass-through taxation avoids double tax

• Good structure for growing service businesses

Cons:

• Payroll requirements

• More strict IRS rules

• Reasonable compensation requirement

Best For: Consultants, agencies, online businesses, service companies, and profitable LLCs.

3. C-Corporation Taxation (Form 1120)

C-Corp is less common for small LLCs but useful for certain growth-focused companies.

C-Corp makes sense when the business:

• Wants to reinvest profits instead of distributing them

• Requires corporate-level tax planning

• Has aspirations to raise investor capital

• Intends to offer stock-based compensation

• Could benefit from lower early growth tax rates

Pros:

• 21% flat tax rate on corporate income

• Better for reinvestment

• Attractive to investors

Cons:

• Double taxation on dividends

• More complex administration

Best For: High-growth startups, reinvestment-heavy companies, businesses seeking investors.

How to Decide: A Simple Decision Framework

Use this three-step approach:

-

Check ownership

• Single member? Consider S-Corp or default disregarded.

• Multi-member? Choose between partnership or S-Corp.

• Foreign owners? Partnership or C-Corp only. -

Review profit levels

• Low profit: Partnership is simpler.

• Medium/high profit: S-Corp reduces taxes.

• High reinvestment: C-Corp may offer advantages. -

Consider long-term goals

• Simplicity → Partnership

• Tax savings → S-Corp

• Growth & investors → C-Corp

How CP 575 Helps in This Decision

Notice CP 575 tells you:

• Default tax classification

• EIN match with IRS records

• Entity type used for all IRS correspondence

• Whether an election has already been made

This ensures your tax planning aligns with IRS-recognized entity status.

If the classification shown is incorrect for your goals, you may need:

• Form 8832 (C-Corp election)

• Form 2553 (S-Corp election)

Conclusion

CP 575 Day 26 Post FI

Today’s lesson is about strategy—knowing not just what form to file, but why each classification impacts your taxes differently. In the next lessons, you’ll learn how to conduct a final compliance check and complete the 30-day CP 575-based filing roadmap.

Previous Post CP 575 Course Day 25 Post

Next Post CP 575 Course Day 27 Post