Pakistan Practical Taxation Course Post 5

Title: Heads of Income Under Income Tax Ordinance 2001 – Complete Overview

Under Pakistan’s income tax law, income is taxed based on its nature, not merely on who earns it. For this reason, the Income Tax Ordinance, 2001 divides income into different categories called Heads of Income.

Understanding these heads is extremely important because each head has its own tax rules, exemptions, and calculation methods.

This post provides a complete overview before we move into detailed practical sections.

What Are Heads of Income?

Heads of income are classifications used by tax law to determine:

• How income is calculated

• Which deductions are allowed

• Which tax rates apply

• How income is reported in tax returns

Incorrect classification of income is one of the most common mistakes made by taxpayers in Pakistan.

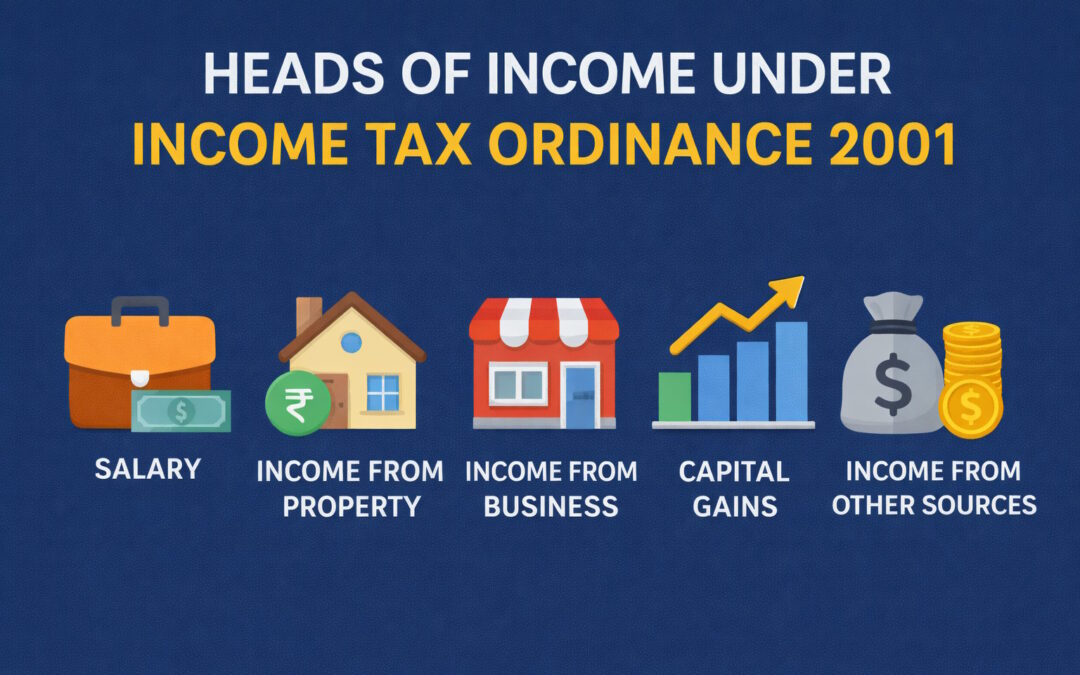

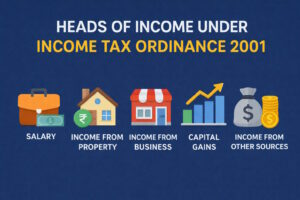

Major Heads of Income in Pakistan

The Income Tax Ordinance, 2001 recognizes the following main heads of income:

• Salary

• Income from Property

• Income from Business

• Capital Gains

• Income from Other Sources

Each head is taxed separately and then combined to calculate total taxable income.

Salary

Salary income includes earnings from employment such as:

• Basic salary

• Allowances

• Bonuses

• Perquisites

• Benefits in kind

Salary income is governed mainly under Section 12 and Section 149, and tax is usually deducted by the employer.

Income from Property

Income from property includes:

• Rent received from house property

• Commercial property rental income

This income is taxed under Section 15 and Section 155 and is very common among individual taxpayers.

Income from Business

Income from business arises from:

• Trading activities

• Manufacturing

• Professional services

• Freelancing and consultancy

Business income is taxed under Section 18 and may be subject to minimum tax or final tax regimes.

Capital Gains

Capital gains arise from the disposal of capital assets such as:

• Sale of immovable property

• Sale of shares or securities

• Sale of mutual fund units

Capital gains are taxed under Section 37 and related provisions, often at special rates.

Income from Other Sources

This is a residual category covering income not falling under other heads, including:

• Bank profit

• Dividend income

• Prize bonds

• Royalties

• Casual or windfall income

These incomes are taxed under Section 39.

Why Correct Classification Matters

Correct classification of income ensures:

• Accurate tax calculation

• Proper adjustment of withholding taxes

• Avoidance of excess tax payment

• Protection from penalties and audits

Misclassification can result in wrong returns, disallowances, and FBR notices.

What’s Coming Next?

Pakistan Practical Taxation Course Post 5 FI

In Post 6, we will begin detailed practical taxation, starting with:

Section 149 – Income from Salary (Complete Practical Guide with Examples)

Instructor

This Practical Taxation Course is prepared and delivered by:

Muhammad Taha Farooq

APFA | ITP

Previous Post Pakistan Practical Taxation Course Post 4

Next Post Pakistan Practical Taxation Course Post 6